Hungary - Country Type

Overview

[reveal]

Hungary is a partner country under the Vienna Initiative NPL framework.

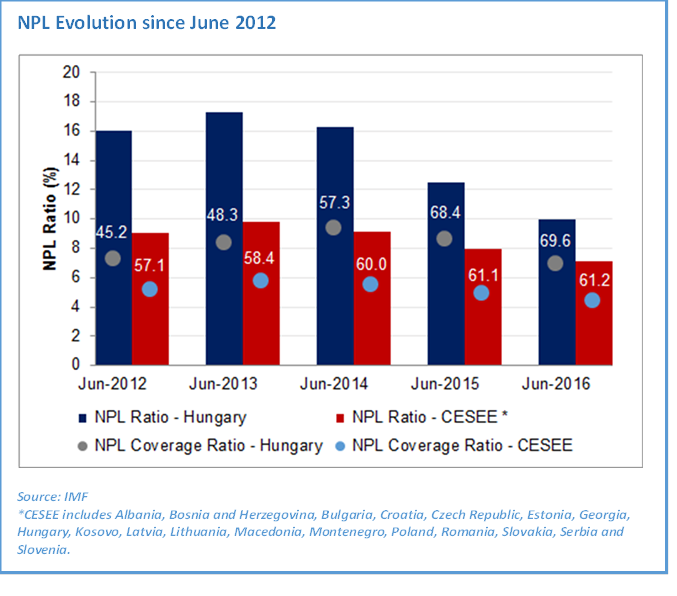

As of June 2016, non-performing loans (“NPLs”) amounted to €4.5 billion, for a NPL ratio of 10% and a NPL coverage ratio of 69.6%.

As part of the Vienna Initiative NPL workstream, EBRD supported the analysis of corporate restructuring and insolvency in Hungary to identify the key obstacles. The government also committed to best practices in resolving NPLs under a Memorandum of Understanding with the EBRD in February 2015. The results of the analysis were presented at a workshop hosted by the National Bank of Hungary ("MNB") in March 2015.

Several measures have subsequently been taken by the Hungarian authorities, such as amending the Personal Bankruptcy Act (September 2015) and the official start of operation of the asset management company MARK (Q1 2016). Further actions are in progress, such as the development of new principles on multi-creditor out-of-court restructuring (‘Budapest Approach’) and a future amendment to the Bankruptcy Act. Regarding the former, a second workshop was held in January 2016 with government officials, bank representatives and legal professionals. EBRD commissioned the production of a report, and the draft MNB recommendation on out-of-court restructuring was presented to banks and industry professionals at a workshop in Budapest in October 2016. The final recommendation was officially issued in June 2017. [/reveal]

Highlights on NPLs (click to enlarge)

![]()

National Bank of Hungary, Financial Stability Report, November 2016

[reveal]The ratio of non-performing loans declined in H1 2016, although further decrease is necessary. So far, the results of the decline are mainly attributable to regulatory measures, in particular to the active role played by the Central Bank. The turnaround of lending also helps to outgrow the problem of nonperforming loans; nonetheless the active involvement of the Central Bank is still necessary, while the steps taken to date continue to urge banks to solve the problem.

The historically robust shock absorbing capacity of the banking sector allows the working off of the legacy of the pre-crisis overheated lending and the cleaning of the non-performing loan portfolio in a decisive manner. While the corporate NPL ratio is still approximately 15%, it can reach the 5% level within the next two years based on the market catalyser role of the Hungarian Restructuring and Debt Management Private Company Limited by Shares (MARK Ltd). In the household portfolio, the conversion of FX loans into forints combined with the low interest rate level considerably reduced the parameters of credit risk, and the share of household loans with over 90 days of delinquency is expected to decrease from the 16% mark as of June 2016 to levels close to 13% in the next two years.

On the other hand, the pick-up in the housing market is not sufficient for a stronger cleaning of the non-performing mortgage loan portfolio. The ratio of non-performing mortgage loans in the banking sector continues to be high in spite of the historically high cleaning ratio (significantly helped by collateral enforcement). Households’ non-performing mortgage loans declined from 20% to 18% year-on-year by the end of June 2016, but this level can still be considered problematic, and the wait-and-see strategy of banks may continue to hinder portfolio cleaning.[/reveal] See full text

IMF, Hungary – 2017 Article IV Consultation-Press Release; Staff Report; and Statement by the Executive Director for Hungary, May 2017

[reveal]While balance sheets have strengthened with progress in reducing NPLs and FX mismatches, it is important to remain prudent to guard against other risks including those that could arise from increased real estate prices. Staff therefore welcomes the strengthening of the macroprudential framework, which is timely as the re-leverage cycle starts to take off. In particular, debt cap rules, which the authorities noted could have helped contain the credit-fueled boom-bust cycle during the global financial crisis, were introduced. The MNB and staff agreed that macroprudential measures should focus on addressing systemic risks. Other concerns such as supply bottlenecks should be addressed directly through structural reforms. The authorities believe that the operational costs of many Hungarian banks are relatively high. Consolidation among the many cooperative credit institutions is expected to continue in 2017. The authorities agreed with staff that consolidation of the banking industry should be market determined. [/reveal] See full text

European Commission, Country Report Hungary, February 2017

[reveal]The banking system has strengthened substantially in the past two years. The sector’s profitability has been helped by the improving economic environment and by a reduction in taxes on banks. Prompted by regulation, financial institutions continued cleaning up their portfolios of non-performing loans.

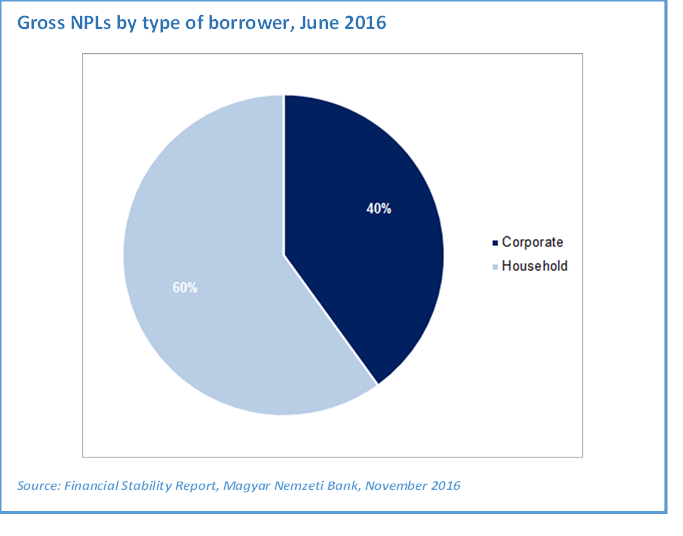

Although declining, the level of NPLs remains high. The NPL ratio peaked in 2014 (Graph 3.2.1). Following the conversion of foreign-currency mortgages and a pick-up in economic growth, also reflected in real estate valuations, banks’ asset quality has been gradually improving. NPL ratios stood at 16.9% and 7.1% in the retail and corporate sectors respectively in the first half of 2016. Although the absolute level is still high in comparison to other Member States, they are well provisioned.

In that context, lending to the private sector is improving, but credit growth remains modest. While banks’ lending capacity is close to a historical high, their willingness to lend remains limited, especially to the corporate sector. Lending is also dampened by their sizeable amount of non-performing loans. The central bank launched various schemes to promote lending to small firms, which picked up significantly in 2016. Lending to households also improved in 2016, as the new government housing support scheme and growing property prices started to spur households’ borrowing. However, overall credit growth is not yet strong enough to support economic growth.[/reveal] See full text

European Investment Bank, CESEE Bank Lending Survey, H2 2016

[reveal]Hungarian banks report that credit demand has been increasing significantly (well above CESEE average) and supply conditions have been catching up. NPL figures have been improving significantly both in the corporate and the retail segments. The improvement is in line with the general developments of NPLs in CESEE, but yet more pronounced. Further progress in the resolution of NPLs is expected in the coming months.[/reveal] See full text

Highlights of significant measures implemented recently

[reveal]

- New recommendation on out-of-court restructuring: Issued for public consultation at the beginning of February 2017 to all financial institutions under Hungary’s Central Bank’s (MNB) regulatory regime and officially came into force in June 2017. The MNB recommendation sets out best practice guidelines on OOCR and consensual settlement of NPLs in the corporate sector. The recommendation is technically non-binding but is expected to have significant power of persuasion and to be an important tool for NPL resolution. The recommendation was first drafted in cooperation between MNB and EBRD.

- Law on enforcement procedure: Law adopted in March 2017 to increase the minimum sale price of a residential property (“property”) in the enforcement procedure from the current 70% to 100% of the market value (i.e. price set by the appraisal of the bailiff), provided that (i) the claim to be enforced stems from a consumer contract; (ii) it is the debtor's only property; and (iii) the debtor resided in that property for at least six months prior to the initiation of the enforcement procedure. If the property cannot be sold within one year, the minimum sale price may be reduced to 90% of the market value. The law also allows the parties to freely agree on a minimum sale price below the 100% threshold, on the condition that the creditor's claim terminates upon the sale of the property and the distribution of the enforcement proceeds (irrespective of full recovery).

- Report on “Analysis of International OOCR and Implementation in Hungary”: Published in Q2 2016 by EBRD with the assistance of EY, this explains the origin of the MNB recommendation issued on OOCR described above.

- Report on “Analysis of Corporate Restructuring and Insolvency in Hungary”: Published in Q1 2015 by EBRD with the assistance of EY and White & Case, this provides an overview of the key impediments to NPL resolution in the corporate restructuring and insolvency framework.

- Amendment to the Personal Bankruptcy Act: The Act, introduced in 2015, simplifies the existing framework and creates an efficient personal bankruptcy system to provide relief to qualifying debtors and at the same time the creditor interests are taken into account. It applies mainly to households whose residence would be subject to enforcement and sale and other over-indebted persons.

- Electronic Sales System (EÉR): Launched on 1st January 2015 as an online platform for selling the assets of debtors in liquidation.

- MARK Zrt: Established by MNB in November 2014 with the mandate to purchase commercial real estate (CRE) exposures from banks to reduce risks inherent in the Hungarian financial system. The design of MARK benefitted from IMF technical assistance, and was ruled free of state aid by the EU Commission in February 2016. MARK is in the process of assessing registered portfolios.

[/reveal]

IMF, Hungary – 2016 & 2017 Article IV Consultation-Press Release; Staff Report; and Statement by the Executive Director for Hungary, April 2016 and May 2017

[reveal]

- Banks with large portfolios of non-performing loans to commercial real estate will be subject to a systemic risk capital charge effective July 2017. Since the announcement of this charge in November 2014 till mid-2016, banks reduced these exposures by about HUF 500 billion (1.4% of GDP).

- The level of the corporate non-performing loans (NPL) significantly dropped in the last two years, and the MNB is finalizing (in line with past staff advice) the sale of its asset management company for commercial real estate (MARK). When MARK started to operate in 2015, more than 20% of the outstanding corporate loans were non-performing, while almost 50% of the commercial real estate loans were in default. At the end of 2016, these ratios came down to 11% and 24% respectively. MARK played a crucial role in jump starting the market for nonperforming commercial assets by improving the quality of information on assets and creating asset management services. MARK’s role, together with the pre-emptive introduction of the systemic risk capital buffer, allowed for a significant drop in the problem portfolio after only 2 years. MARK will now be operated by new private owners after the closing of the ongoing sale at end-June, will only rely in external private funding for the potential purchase of NPLs to avoid MNB monetary financing.

- The new Personal Insolvency Law is a step in the right direction to reduce the uncertainty and costs of resolving debt of natural persons as well as to offer them a second chance, but its effectiveness is yet to be tested. The first phase became effective September 2, 2015, and applies to households whose dwelling would be subject to enforcement and sale, while other over-indebted persons will be covered effective October 1, 2016. This phasing is intended to give priority to those in most need and to reduce the administrative challenges. The procedures are complex and consideration is being given to streamline them and later, as experience is gained, to review the law.

[/reveal] 2016 full text and 2017 full text

European Commission, Country Report Hungary, February 2017

[reveal]The government committed to gradually reduce bank taxes, to reprivatise two commercial banks recently acquired by the Hungarian state, and to assist in reducing non-performing loans. Measures have been taken to address bad household debt. Delinquency rates are high among household mortgage borrowers (close to a quarter of mortgages are classified as NPL). The Hungarian Asset Management Company, with capacity to purchase a total of 35 000 dwellings, is targeting non-performing debtors in the most difficult financial situation. Mortgage holders who are excessively indebted can also initiate a debt settlement procedure under the Personal Bankruptcy Act adopted in 2015. Debtors have in general improved cooperation with lenders. This was helped by a recommendation issued to credit institutions by the central bank. The latter determined the expected minimum framework of cooperation between debtors and creditors.

Important steps were also taken to tackle nonperforming corporate loans. The asset management company established by the central bank (MARK) officially started operating in 2016. It aims to tackle the sizeable number of distressed commercial real estate loans and more generally to initiate the clean-up of banks’ balance sheets by selling their non-performing portfolios on the market. The central bank is also working on a new recommendation which will set out best practice guidelines on out-of-court restructuring and consensual settlement of NPLs in the corporate sector. The recommendation is designed to encourage lenders to adopt a more cooperative and coordinated approach where more than one financial creditor is involved. It could become an important tool for resolving such loans and improve the depth of the market for distressed assets in Hungary.[/reveal] See full text

EBRD, Strategy for Hungary, March 2016

[reveal]EBRD will also continue its cooperation with the Government and the Hungarian National Bank (MNB) as they take steps to enhance the legislative and institutional framework in support of NPL resolution. In this context, the Bank will continue to provide policy advice and technical assistance to enable faster and more efficient NPL resolution under the Vienna Initiative. Amongst others, EBRD will:

- Seek opportunities to finance distressed assets across sectors to assist with NPL resolution and freeing up banks’ capacity for new lending.

- Continue its ongoing technical assistance, under which legal and financial obstacles to corporate restructuring and NPL resolution have already been diagnosed. Based on this work, the MNB has requested EBRD assistance on a new bankruptcy law, and on private out-of-court restructuring principles. Other work with the Hungarian authorities will draw on the recommendations made by the working group of public and private sector stakeholders, using the Vienna Initiative’s platform.

- Continue advising, as requested, on the governance of the AMC, and on portfolio sales and restructuring efforts by this entity. Advice would be clearly separated from any potential Bank interest in investment in portfolios sold by the AMC.

- Assist with establishing a securitisation platform.

[/reveal] See full text

Government of Hungary, National Reform Programme 2015 of Hungary

[reveal]

- Several barriers impeding fast and efficient portfolio cleaning were identified. One of the main impediments, particularly in the commercial real estate segment, is the subdued demand coupled with over-supply, which contributes to significant frictions in the distressed debt management market. MNB is cooperating with the EBRD on possible recommendations to address this issue.

- As regards corporate NPL, MARK Hungarian Restructuring and Debt Management Ltd. established by the MNB in November 2014, is going to target commercial real estate exposure with the aim of reaching a significant drop in corporate NPL.

- The Electronic Sales System (EÉR) was launched on 1st January 2015. EÉR provides an online platform for selling the assets of debtors in liquidation. Routine use of EÉR means to ease the administrative burden, the review of auctioned assets and the comparison of prices. Under the liquidation process, such assets (complete production units, real estate, etc.) are sold at a reasonable price that serve as a beneficial purchasing opportunity for production and service companies, which indirectly has an impact on businesses to stimulate and support them, and also to promote investment and maintain jobs. The anonymity of the application/bidding is expected to increase the price of assets, and may lead to higher return ratio of creditor claims.

[/reveal] See full text

MNB-EBRD workshop in Budapest – OOCR Recommendation: practical applicability and MNB’s expectations, October 2017

[reveal] On 12 October 2017, the Magyar National Bank (MNB) hosted a workshop in Budapest to foster adoption of the new out-of-court restructuring recommendation (OOCR Recommendation) it officially issued in June 2017. The event, jointly organized by MNB and EBRD under the NPL work stream of the Vienna Initiative, brought together leading banking groups operating in Hungary, as well as financial and legal advisors and representatives from local authorities.

The workshop is the continuation of a fruitful collaboration initiated over two years ago between the MNB and the EBRD to address the NPL challenge in Hungary. Hungary has taken positive steps to reduce its stock of bad debt, with the NPL ratio recording a significant drop to 5.4 per cent as of June 2017, according to IMF data (against 12.5 per cent two years earlier). In June 2017, the MNB officially issued the OOCR Recommendation (which was drafted under the guidance and technical support of the EBRD). The workshop was designed to promote the use of the OOCR Recommendation, which is expected to lead to greater cooperation between banks on corporate restructuring, but also on consensual settlement and enforcement of security out of court. The workshop also highlighted that further reforms to address NPLs were needed, in particular in the areas of (i) bankruptcy framework, (ii) skills in judiciary system as well as in bank workout units and (iii) alignment with and implementation of new EU regulations on NPLs.

[/reveal]

[reveal] Additional information:

- Press Release

- Workshop Agenda

- Presentations

- Evolving European regulatory landscape for NPLs: how to prepare - E. Cloutier, EBRD

- The legal interpretation of the OOCR Recommendation - S. Mestyán, Lakatos, Köves and Partners [/reveal]

Central Bank of Hungary and EBRD conclude workshop on NPL resolution, March 2015

Piroska M. Nagy (EBRD) and Ádám Balog (MNB)

[reveal]The Central Bank of Hungary (MNB) and the European Bank for Reconstruction and Development (EBRD) held a prominently attended workshop, on 3 March 2015, under the Vienna Initiative on ways to assist banks’ and the authorities’ efforts at the resolution of NPLs through concrete and sustainable actions. Leading bank groups operating in Hungary, potential investors and IFIs discussed the legal, tax and regulatory environment in Hungary for NPL resolution. The participants also examined in-house NPL management, including out-of-court restructuring and ways to facilitate sales of corporate NPL portfolios as well as experiences with asset management companies (“bad banks”).

Follow-up actions identified during the workshop include:

- Re-examine the existing licensing requirement for NPL purchasers in line with other countries in the region.

- Considering tax relief and other incentives for banks and debtors for cancellation of debt and debt for equity swaps in a restructuring context.

- Greater cooperation among banks to promote early out of court restructuring and applying the Budapest corporate restructuring principles.

- Considering a more significant role for banks as creditors in the bankruptcy (reorganisation) procedure as well as in the liquidation procedure and the appointment of the insolvency office holder.

- Using the recently established asset management company on a fully commercial basis with strengthened governance to promote a secondary market for NPLs.

For more information on the event and its outcomes, please click on the links below.

Meeting Programme and List of Participants

Analysis of Corporate Restructuring and Insolvency in Hungary – Final Report

Presentations:

- NPL resolution: a macro view – G. Fábián, MNB

- NPLs in Hungary: a regional perspective – J. Roaf, IMF

- Analysis of Corporate Restructuring and Insolvency in Hungary – EBRD, White and Case and Ernst & Young

- EBRD & The Central Bank of Hungary – A. Rawal and A. MacCallum, Alvarez & Marsal

- Asset Management Companies: Observed best practices – Martin Rauchenwald, Oliver and Wyman

- What Role for “Bad Banks”: A perspective from Slovenia – M. Mavko, EBRD & DUTB

- Corporate NPL Sales: the role of specialist investors – P. Le Baquer, Rothschild

[/reveal]